PSAOs, a middleman to handle middlemen

Independent pharmacies rely on PSAOs to negotiate with PBMs. It's as messy as it sounds.

This newsletter continues a thread from two weeks ago, about the U.S. pharmacy sector and why it’s so challenging to innovate (see the first part here).

After I started researching how someone could start a consumer-oriented specialty pharmacy, someone suggested that leveraging PSAOs might work. I had never heard of a PSAO; you might not have either.

“PSAO” stands for “pharmacy services administrative organization.” It’s essentially a group contracting organization for independent pharmacies, allowing them to amass enough power to negotiate effectively with PBMs, using the PSAO vehicle.

The theory re: launching a new specialty pharmacy is that, by contracting directly with PSAOs, a new specialty pharmacy could avoid having to direct-contract with insurers or PBMs, many of which have their own specialty pharmacy and are unlikely to contract with competitors.

So with that, I started to look into PSAOs. And I’m here to tell you that, like most things in health care, the these groups seem to have started from a good place and devolved into a morass of overlapping contracts, questionable business practices, and consolidated, overly powerful entities. (But they still might provide a leverage point for a new specialty pharmacy.)

How PSAOs fit into the overly complicated pharmaceutical system

Independent pharmacies are too small to wield significant negotiating power one-on-one with huge PBMs and insurers, so they can band together under the PSAO structure to get more favorable terms. This arrangement is also easier on PBMs—they only have to coordinate with a few entities, instead of thousands.

And, in case you’re not familiar with the weird, wild world of drug purchasing: PBMs are the middlemen between retail pharmacies, insurers, and drug manufacturers. To describe this relationship, I’m going to bring in three charts that start complicated and…get more complicated.

This first, most simple chart, shows the flow of drugs through the system.1 “Wholesalers” here = group purchasing organizations, or the bulk purchasers that supply outpatient, retail pharmacies as well as inpatient, hospital- and clinic-based pharmacies. GPOs are, ahem, not great.

You’ll note that PBMs are not in this chart. That’s because they don’t actually handle drugs themselves; they’re not a part of the physical supply chain.

Source: http://www.americanhealthpolicy.org/Content/documents/resources/December%202015_AHPI%20Study_Understanding_the_Pharma_Black_Box.pdf

Okay, so now enter PBMs, which are part of the financial chain of drugs.

For a quick diversion into how PBMs fit into the financial chain, proceed with the following paragraphs. If you value your time and brain cells, just skip this.

🤓 You can see in the following chart that PBMs link to the drug manufacturer, pharmacy, and health plan/insurer—but not the wholesaler.

That’s because—in a strange (but not unexpected, if you’re familiar with how health care works) twist, pharmacies pay wholesalers one price (the Wholesale Acquisition Cost, or WAC), and then PBMs pay a negotiated reimbursement to pharmacies. PBMs and wholesalers don’t have to interact.

You may also notice in the following chart that the payments process involves a lot of acronyms. Pharmacies pay wholesalers the WAC, but PBMs reimburse pharmacies using a different drug formula altogether—in the chart example: [AWP – 15%] + 2. AWP stands for “average wholesale price,” or the price that the manufacturer decides is fair. AWP is also known as a list price or reference price, although my favorite descriptor comes from a report: “It is important to understand that AWP is not a real ‘price’” (emphasis mine).

As a rule of thumb, the AWP is usually ~20% more than the WAC. The difference between the WAC and the AWP is known as the “spread,” and that’s how pharmacies make a large portion of their revenue; pharmacies want [the negotiated payment from the PBM (based off the AWP) + the patient’s copay] to = more than the WAC.

PBMs, meanwhile, make money on a different kind of “spread”: the spread between what they get paid by the insurer, and what they have to pay the pharmacy (which is, again, based on the AWP).2

Source: http://www.americanhealthpolicy.org/Content/documents/resources/December%202015_AHPI%20Study_Understanding_the_Pharma_Black_Box.pdf

In short: PBMs are middlemen.

You know what else the pharmaceutical space needs?

If you said another middleman, congrats, you have a prosperous future in the bowels of health care.

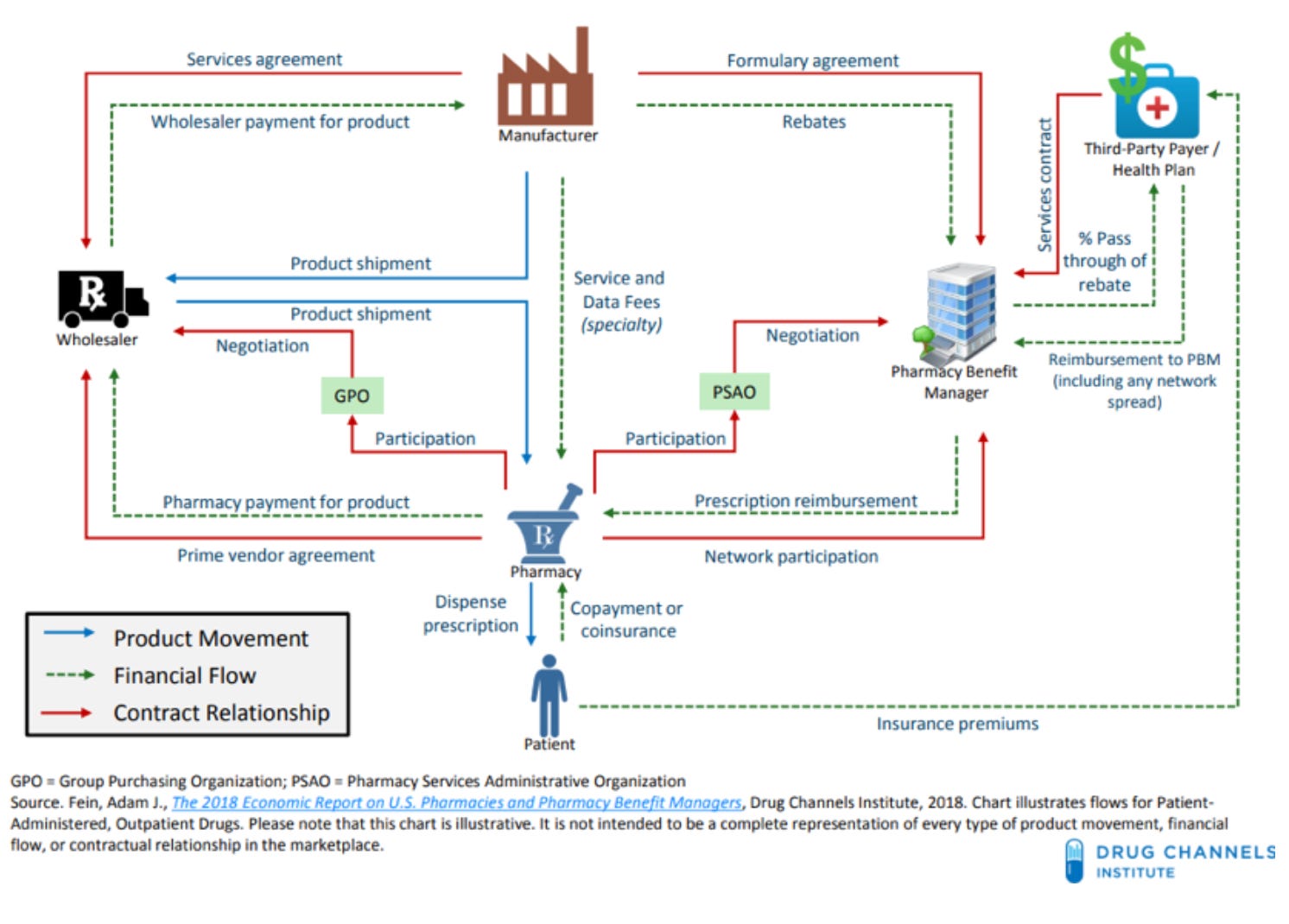

PSAOs are the middlemen for the middlemen, or an entity that fits between PBMs and pharmacies:

Source: https://drugchannelsinstitute.com/files/2018-PharmacyPBM-DCI-Overview.pdf

PSAOs negotiate with PBMs on behalf of independent pharmacies.

In defense of PSAOs

Ok, look, PSAOs make a bad drug chain worse. At the same time, I can’t blame independent pharmacies for wanting to band together to have more power against PBMs. After all, PBMs are highly concentrated, and they’re increasingly owned by just a few insurers (which, editorial note, diminishes their incentive to actually negotiate on behalf of patients, because they’re increasingly playing with house money).

Bringing back this delight of a chart. Source: https://www.drugchannels.net/2019/12/insurers-pbms-specialty-pharmacies.html

Independent pharmacies keep getting kicked around. PBMs have soaked up enough power that they can (and do) impose “take-it-or-leave-it” contracts that force independents into accepting rates that may not be enough to cover the cost of the medication. PBMs aggressively audit independent pharmacies, reserving the right to remove them from plan networks over small administrative errors (a fact that cannot be untied from PBMs’ close relationships with chain pharmacies). It’s an aggressive relationship with a significant power differential.

All of this, even though independent pharmacies are a net good for the U.S. They hire pharmacists and other workers, often in rural or remote areas, and they tend to treat their employees far better than CVS (which got caught pushing its pharmacists past their breaking point, dispensing as many drugs as possible).

Independent pharmacies can provide a small business opportunity for immigrants or enterprising individuals. And they’re absolutely crushing the vaccine rollout—particularly compared to CVS and Walgreens—as seen in West Virginia and South Dakota’s blazingly fast early vaccine campaigns.

All of this to say, if independent pharmacies want to contract together against PBMs, what could go wrong?

Well…

Why PSAOs could be good but functionally hurt pharmacies

…it turns out that most PSAOs are owned by huge OTHER middlemen (ding ding, wholesalers/GPOs).

The largest PSAOs, according to a recent article by Adam Fein at Drug Channels, are:

Health Mart Atlas (HMA), owned by McKesson

LeaderNET, owned by Cardinal

MSInterNet, owned by Cardinal

Managed Care Connection, owned by Cardinal

Elevate Provider Network, owned by AmerisourceBergen

Arete Pharmacy Network, a member-owned cooperative and one of the only PSAOs not owned by a GPO

This wouldn’t necessarily be bad, except it means that the theoretical banding-together of independent pharmacies against concentrated power is…happening on the terms of concentrated power.

Case in point: A 2013 GAO report on PSAOs found that some wholesalers use their power over independent pharmacies to require the pharmacies to also use the wholesalers’ unrelated business lines (i.e., the GPO portion of the business).

Some wholesalers actually seem to be running PSAOs solely to drive business back to their group purchasing operation. The GAO reported that “Only 1 of the 10 PSAO owners we spoke with stated that its PSAO service was profitable…it may be the case that offering PSAO services may benefit the owner’s non-PSAO line of business even if the PSAO service itself is not profitable.”

I’m not trying to allege suspicious behavior where none exists (except it sounds suspiciously like tying to me); instead, I’m trying to emphasize how little power independent pharmacies have. Even when banded together, they’re at the mercy of McKesson.

Independent pharmacies’ lack of power in dealing with their PSAO owner comes out in surprising ways. Some PSAO contracts allow the PSAO to adjust pharmacies’ payments even after sending the payments, and sometimes without letting pharmacies know. Many of these contracts also have dispute resolution requirements, making it more challenging for small pharmacies to fight unfair treatment in court. And the PSAO contracts can be far too confusing for a small staff with an expertise in pharmacy, not contracts.

And…PBMs still have too much power

Network aggregate reimbursement

The PSAO may aggregate independent pharmacies’ negotiating power, but it doesn’t protect them from PBMs. Under a contract term called “network aggregate reimbursement,” PBMs can combine all prescription claims for all the pharmacies in one PSAO, then reimburse them in aggregate—meaning that different pharmacies in the same PSAO may receive different amounts of payment for the same drugs.

As Melanie Maxwell, the Senior Vice President of an organization that negotiates contracts for independent pharmacies, told an industry site, “The PBM can reimburse the pharmacy at any rate it deems appropriate as long as overall reimbursement for all claims billed by all PSAO pharmacies for the entire year combined equal the rates stated in the contract.” Which is…not how any other business works.

Retroactive payments

PBMs can also pull back money they’ve already paid pharmacies, and PSAOs have limited power over it (unless the PSAO preemptively negotiates a contract banning such practices).

In 2018, OptumRx and CVS changed their contracts with EPIC Pharmacies, a PSAO representing 1,500 pharmacies nationally, adding a payment adjustment clause allowing Optum and CVS to pull back money already sent to EPIC members. EPIC, a rare member cooperative, responded by withholding significant amounts of reimbursement in escrow, to ensure that member pharmacies had the money available to send back. But this meant that some pharmacies didn’t have access to tens of thousands of dollars that they were expecting in reimbursement, an unexpected change that upended their businesses.

Stock photos doing it again with this insanely creepy photo of a CVS

According to one independent pharmacist quoted in the Columbus Dispatch, the whole situation was “just one more level of non-transparency…I don’t know who is making the money, but it’s easier to hide money, easier to steal money.” At least one law firm, Frier Levitt, seems to have regular business (at least up until 2020) representing independent pharmacies against PSAOs that hold funds in escrow. And industry websites now strongly recommend independent pharmacies ensure that PSAOs negotiate firmly with PBMs and prohibit such clawbacks.

Conclusion

It’s genuinely really frustrating to see so many parts of health care be…bad. From a pure business perspective, each of these choices makes sense. All of the companies involved are engaged in a complicated arms race against each other and the perpetual consolidation of the system. And, unsurprisingly, the smallest entities that have the closest connections to patients are the ones that get left behind.

I also suspect that most of these organizations get away without legal or regulatory scrutiny because they’re just so confusing. If the FTC or DOJ stopped UnitedHealth from acquiring everything in its path, maybe independent pharmacies wouldn’t have to rely on PSAOs to do their negotiating. If lawmakers were paying attention to the close association between GPOs owning PSAOs and requiring PSAO members to also use GPO services, perhaps that could be prohibited. Instead, under the status quo, UnitedHealth can crack down on small administrative errors and kick independent pharmacies out of network, while UnitedHealth itself continues to consolidate power.

This post focuses on non-specialty drugs. Specialty drugs have some overlap with the system mentioned here, but not entirely. I wrote a little bit about specialty drugs here, although there’s always more.

I am…not an expert on this. Let me know if I got something wrong!