This week, Mark Cuban announced the launch of the confusingly named Mark Cuban Cost Plus Drugs Company (MCCPDC).

(Sorry, I had to.)

The company’s business model is to cut out the major middlemen, PBMs and GPOs, in the pharmaceutical supply chain and source drugs directly, providing certain medications to patients for a comparatively cheap price.

Cutting out the middlemen

This isn’t a bad idea, especially because PBMs and GPOs have contributed greatly to the fragmentation and expense of the drug market in the U.S.

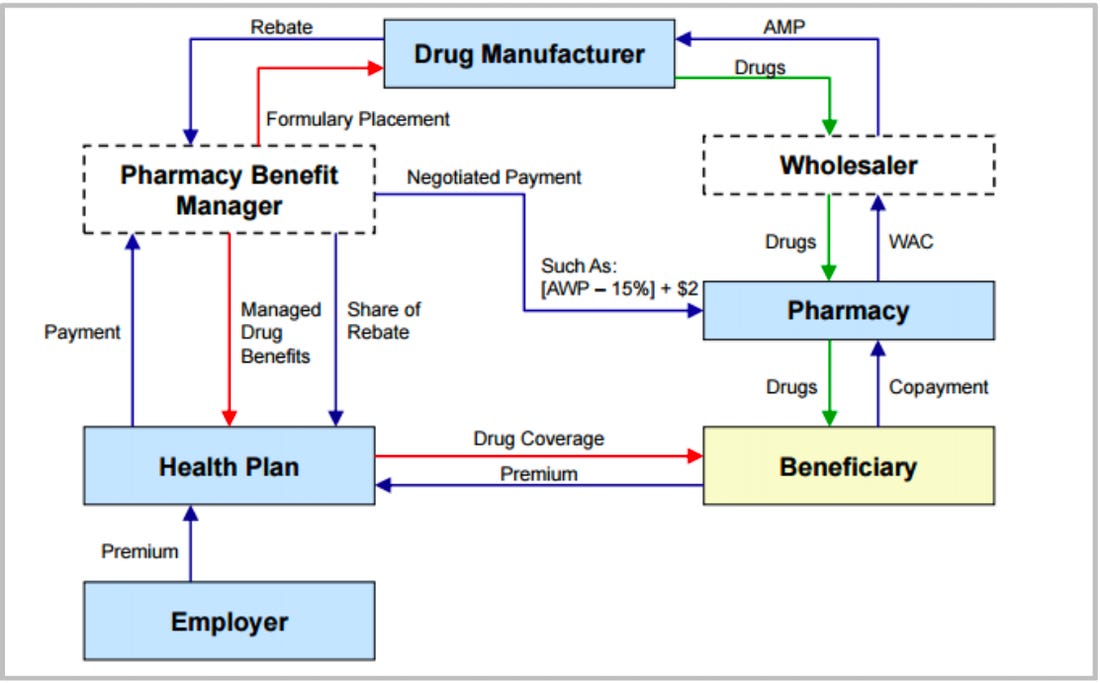

This first, most simple chart, shows the flow of drugs through the system…

You’ll note that PBMs are not in this chart. That’s because they don’t actually handle drugs themselves; they’re not a part of the physical supply chain.

GPOs, or group purchasing organizations, are represented in the charts above as wholesalers. GPOs act as middlemen distributors between manufacturers of commoditized medical supplies, including generic drugs, and the providers who buy them. GPOs certainly serve a function—it would be very complicated for a hospital or office to manage all of the contracts and deliveries separately—but GPOs have also become oligopolized behemoths that contribute to fragile supply chains and therefore basic product shortages. More about GPOs here, from The Prospect, if you’re interested.

(There’s actually ANOTHER middleman involved in drug transactions, and those are PSAOs, originally intended to give independent pharmacies more negotiating leverage. In practice, most of the biggest PSAOs are actually owned by GPOs. Really there’s just a few companies at the top. I wrote more extensively about PSAOs here.)

All of this to say that the drug purchasing and supply chains are complicated and dominated by a few companies that thrive off that complication.

How MCCPDC began

Enter the Mark Cuban Cost Plus Drugs Company.

As founder and CEO Alex Oshmyansky told the ZDoggMD Show, MCCPDC originally started as a nonprofit (the name of which seems to have been lost forever, although believe me, I tried to find it) to channel Oshmyansky’s rage at the arbitrariness of drug pricing following the Martin Shkreli incident.

Oshmyansky, however, ran into the problem that many nonprofits run into, which is that he couldn’t find enough funding. Eventually he went to Y Combinator, a well-known startup incubator, and asked to be one of the few nonprofits they sponsor every year. Instead, they encouraged him to switch the model to a public benefit corporation and then invested.

At some point, at least according to the founding narrative, Oshmyansky cold-emailed Mark Cuban, and the rest (including whatever was almost certainly a more modest company name) is history. Cuban invested an unknown amount and is now closely involved in the company.

The specifics of the company itself seem to be in flux, which I attribute to its newness. According to its website and press release, MCCPDC is a PBM and therefore negotiates with drug manufacturers directly. Unlike traditional PBMs, MCCPDC has publicly stated that its prices will be determined by a comparatively transparent formula: manufacturer’s cost + 15% margin + $3 pharmacists fee.

MCCPDC has also announced its disdain for the PBM rebate system, so it seems they won’t be seeking rebates. (Not that manufacturers would be breaking down the door to offer rebates, at least at first—rebates are typically offered as an inducement by manufacturers to get more expensive drugs included on a PBM’s formulary so that associated insurers will cover it. MCCPDC is cash-only at the moment, so there’s a built-in ceiling for how much patients can pay and therefore less incentive for rebates to be involved at all.)

In the last year, it seems, MCCPDC decided to partner with Truepill to build and manage the customer interface (the website), the prescription fulfillment, and delivery. MCCPDC most likely deals primarily or exclusively in negotiations with manufacturers.

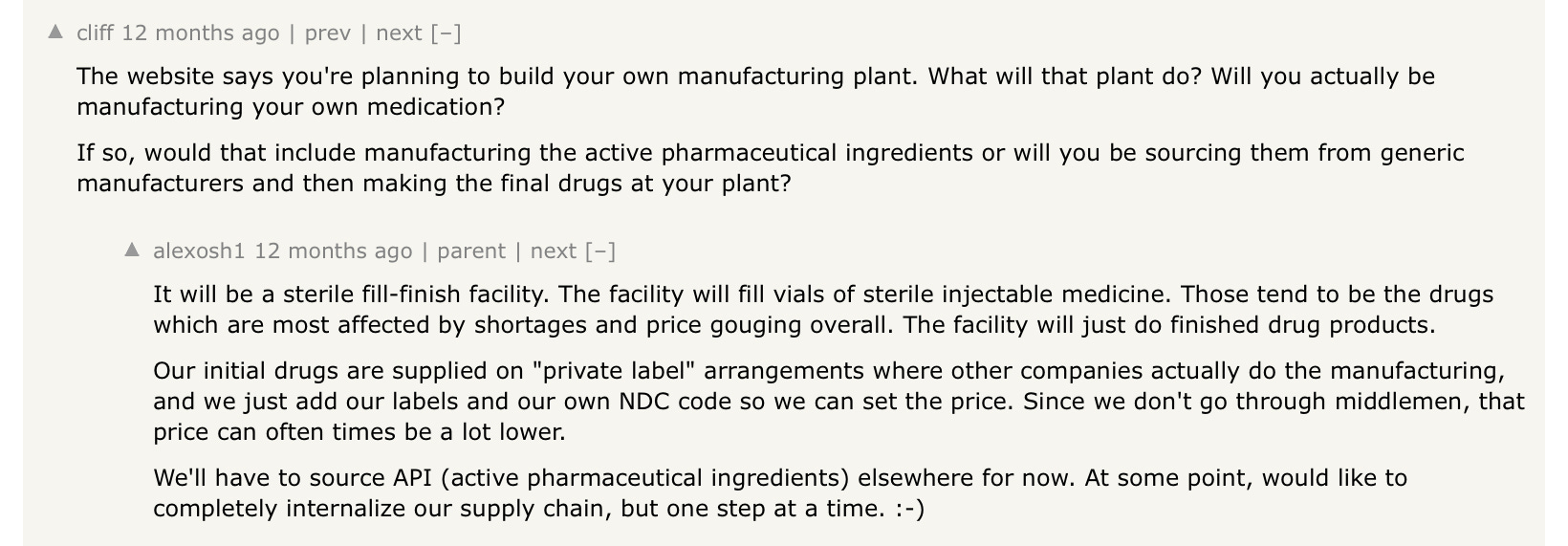

At the same time (and this is where the ambitions get fuzzy to me), MCCPDC is building its own drug manufacturing plant in Dallas, slated to open by the end of 2022. Originally, in a post to Hacker News (I went deep on researching this), Oshmyansky said the plant would be focused on fill-finish, one of the last steps of the drug manufacturing chain for injectables, where the liquid drug is sterilly inserted into vials. (In 2020, fill-finish was expected to be a big roadblock to fast vaccine production, as there are only a few plants worldwide that can handle this step.)

In more recent communications, Oshmyansky has referred to the plant in less specific terms, making it sound more like it will be involved in generic drug production, rather than fill-finish.

If I had to guess, there may have been some government or company inducements to build a fill-finish plant that fell away after the vaccines were widely distributed within the U.S., and now the plant will be involved in more general manufacture.

Part of a trend

Why does all of this matter? (Maybe you aren’t asking this, but I was asking myself, as I dug through old message board posts.) First, I think it’s interesting to see how a company evolves, even one that’s trying to tackle such a well-known, decades-old problem as American pharmaceuticals. Second, while MCCPDC is unique in its name, publicity, and scope of intention, it is not the first to decide that the only way to fix the pharmaceutical system is to...go around it.

Civica Rx

Civica Rx, another run at this problem from a hospital, rather than consumer, angle, is a nonprofit funded by a group of several health systems to guarantee bulk drug availability.

As briefly mentioned above, because of the volume that they purchase, GPOs are more or less capable of setting the prices for certain generic drugs. They’ve driven the price down so low that manufacturers have been forced to offshore their production lines, use cheaper ingredients, and spend less on inventory and maintaining a redundant supply chain. The result is that hospitals have suffered recurrent waves of generic drug shortages. At the same time, some drugs are priced far too high.

Civica Rx aims to solve the problem by guaranteeing bulk purchases of drugs from manufacturers that can guarantee supply. It’s simple but seems to be working so far; as of July 2021, the organization sells to hospitals comprising more than 30% of all U.S. inpatient capacity and maintains a consistent inventory of medications even during the fluctuations of the pandemic.

EmsanaRx

Tackling the issue from an employer angle is the Purchaser Business Group on Health, a coalition of employers, which recently launchedEmsanaRx. EmsanaRx is a PBM built on transparency for employers, although there’s not a ton of information available publicly. My guess is that it works similarly to MCCPDC for employers.

GoodRx

There’s also GoodRx, which offers coupons and allows consumers to find pharmacies selling certain drugs for lower prices. Although GoodRx has been quite successful and performs a useful service, it’s not so much going around the existing system as leveraging the loopholes within it. GoodRx doesn’t totally fit my theme here—but it is trying to make drug prices more transparent for the consumer, so I decided to include it.

Conclusion

The MCCPDC name belies the seriousness of the company’s intentions: to circumvent and supplant existing PBMs. The model is simple and transparent (once you understand the role PBMs and GPOs play), and it has an element of sticking-it-to-the-man that’s appealing.

Over time, I’ve gotten more skeptical of business models that aim to “disrupt” some core element of healthcare. In all likelihood, eventually that company will find itself seeking to partner with the entities it formerly scoffed at; the legacy system is just too entrenched.

That said, Civica Rx’s initial results have been good, and there’s no reason MCCPDC can’t achieve lower generic drug prices for its cash-pay customers. The part I’ll be interested in watching will be version 2, or what happens when MCCPDC makes moves into insurance-covered patients, providing more complex drugs, and/or manufacturing generics.

This information shouldn’t be taken as investment advice (obviously), and the opinions expressed are entirely my own, not representative of my employer or anyone else.

I always appreciate a clear summary of the complexity of the PBM/drug space, thank you.

Sharing in case you didn't come across this video in your research--it's interesting to compare what has changed vs. what hasn't about his plans from the view Mark shared at the HLTH conference in 2019: https://www.youtube.com/watch?v=4QmYnQnQRd4

I always appreciate a clear summary of the complexity of the PBM/drug space, thank you.

Sharing in case you didn't come across this video in your research--it's interesting to compare what has changed vs. what hasn't about his plans from the view Mark shared at the HLTH conference in 2019: https://www.youtube.com/watch?v=4QmYnQnQRd4

Just did a price check this morning against a key competitor for the new company...

Mark Cuban Cost Plus (90 Day Supply)

Atorvastatin 20mg $5.70

Allopurinol 300mg $9.30

Lisinopril 20mg $6.60

Shipping $5.00

Total: $26.60

Walmart (90 Day Supply)

Atorvastatin 20mg $38

Allopurinol 300mg $51.66

Lisinopril 20mg $10.00

PU@Pharmacy

Total: $99.66