GLP-1s are propping up virtual care startups

What happens when the compounding stops?

Last week, it was announced that Thirty Madison, one of the trifecta of big DTC companies (the others being Hims and Ro), was acquired by Remedy Meds, a company that seemingly came out of nowhere, for a mere $500 million. I’m not sure what Thirty Madison’s most recent valuation was, but when I was an employee there, the company raised a Series C with a valuation of $1 billion — so this acquisition definitely wasn’t an upgrade. What happened?

During the Covid era, a lot of startups raised money on the promise of “virtual care,” the idea that patients could access a lot of what they needed virtually. This obviously had a lot of appeal during a time when everything from weddings to live music events were held virtually, but these startups raised at valuations that implied they expected this to be the future of care. I also explicitly said I expected this to be the future of care. That was wrong!

It turns out that many, many patients continue to see their primary and specialty physicians in person, or see them through telehealth (which is a different model than virtual specialty care, and one that I would argue that health systems have largely begun to figure out), or use urgent care when they need to be seen quickly. This seems like it will continue. I’ve been wrong before (see above), so maybe this will change over time. Unfortunately, it is not changing quickly enough for some of the DTC companies that raised during Covid.

Is GLP-1 compounding propping up all of these companies?

Thirty Madison reportedly faced profitability, operational, and leadership challenges earlier this year and began narrowing its focus to women’s health and hair loss. At the time, Axios’s Erin Brodwin noted, “Thirty Madison is staring down a missed opportunity to own the GLP-1 space, where both Ro and Hims have successfully cashed in.” It did indeed miss this opportunity (although I kind of respect the choice).

In the end, Thirty Madison sold to a company that apparently makes its money doing…GLP-1 compounding.

(Thirty Madison’s Nurx announced in April that it formed a partnership with Eli Lilly to offer Zepbound on-label — meaning specifically for FDA-approved uses, a stricter standard than many of the other GLP-1 telehealth providers are following.)

As I wrote in June, telehealth is a commodity — but so is, increasingly, a lot of virtual care as well: “I was wrong in thinking that many companies would continue to be differentiated; many are…offering prescriptions as a service. The drugs aren’t addictive (except, ahem, for Done and Ahead, rip), but they’re more or less a prescription mill. There are, of course, exceptions.”

In short: I really thought virtual care was going to do more care and less prescribing.

GLP-1 compounding on a dare

For companies that are relying on prescribing to stay afloat, GLP-1s must have been a godsend. Not only are they for a condition that people are used to paying a lot for out of pocket (overweight and obesity), but the FDA declared GLP-1s to be in shortage in 2022, opening the door to compounded GLP-1s.

GLP-1s are largely on-patent still, meaning that companies like Novo Nordisk and Eli Lilly have the exclusive right to manufacture and sell Ozempic and Zepbound. But when a drug is declared to be in shortage by the FDA, that means compounding pharmacies can manufacture similar formulations themselves (I go into greater detail in my compounding article).

But in April 2025, the FDA declared these drugs to be no longer in shortage, meaning continuing to compound them commercially is…no longer allowed!

If GLP-1s are propping up virtual care startups right now, these startups are dependent on the ongoing ability to compound these drugs. And indeed, these startups have continued to compound, despite the legal gray area in which they now find themselves. Novo Nordisk and others have tried various soft power tools to get them to stop, but they haven’t.

I recently came across this newsletter, GLP-1 Digest, which helpfully laid out the next step that Novo Nordisk has to take to address rogue GLP-1 compounders. In short, Novo Nordisk, which owns the patent for Ozempic, seems to be relying on the FDA for enforcement, but the FDA is understaffed. Novo Nordisk could escalate and sue compounders for patent infringement, but as GLP-1 Digest points out, such suits are risky. The startups compounding GLP-1s seem to be daring Novo Nordisk to take such a step.

Quality concerns

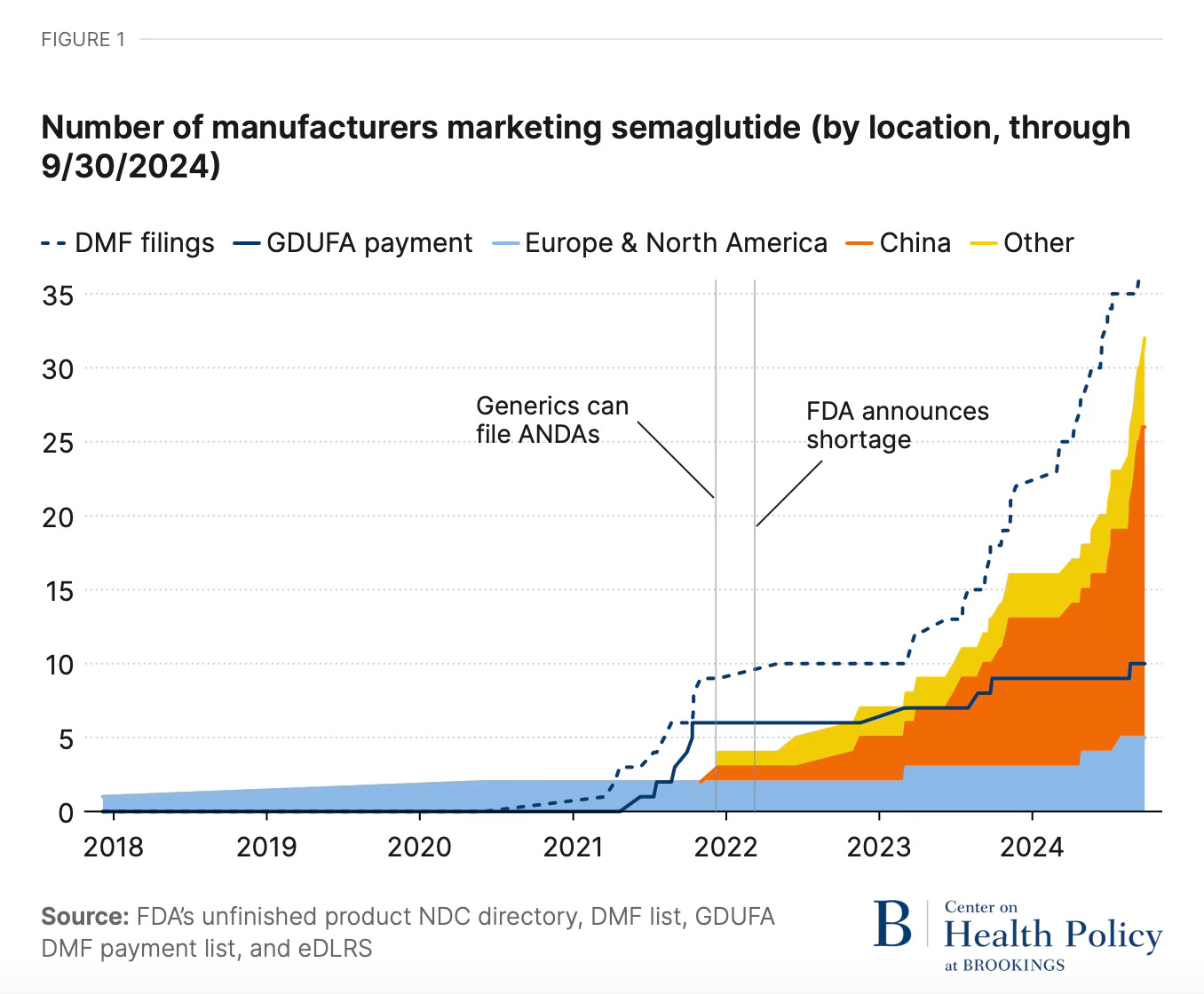

Of course, compounding drugs isn’t necessarily the most patient-friendly option, even if it is cheaper! GLP-1 Digest reproduced this graph from Brookings, which puts a visual to the point I made in my compounding newsletter — the API for compounded semaglutide is coming in bulk, largely from China, and it’s not receiving the same quality oversight and scrutiny that Americans expect from the drug supply chain.

Hopefully Hims and Ro are carefully monitoring their supply chains, but it can be difficult to track where API comes from — even the FDA doesn’t know exactly where most API comes from.

Commodity telehealth and patient front doors

But back to my original question: does any of this commodity telehealth have a future? I wrote back in 2021 that the way to differentiate was through having a patient front door:

Where and how a patient gets care is guided by the “front door,” a term for the patient journey from deciding to explore care options to actually accessing care. Traditionally, the front door was the patient’s primary care doctor, who guided the patient through care and/or referred them to a specialist. Now that primary care doctors are no longer the gatekeepers they once were, the journey has become much more fragmented.

Digital health companies, however, have the opportunity to remodel the front door. [...]

Telehealth PaaS [platform-as-a-service] companies have a lot of market share and a big pool of patients…but they don’t have a front door so much as an open-air marketplace. Patients are left to decide what services they need and what kind of doctor can provide those services, even before they have to schedule the appointment and remember to log into the app. [...]

Other companies build their digital front door around condition-specific marketing and an integrated care model that bundles a large portion of the care for that condition.

But having a front door wasn’t enough for Thirty Madison. The traditional patient front door, after all, is physician referrals — and physicians don’t exactly refer to virtual specialty care companies. Maybe virtual specialty care will ultimately be reserved for care that’s slightly outside the mainstream? By that, I mean companies like Parsley or Function Health. Or maybe it’ll continue to be for the big things that people google — sexual function, weight control, and hair loss. (But, perhaps, at lower valuations than the virtual specialty care companies once commanded.)

I don’t know, but I’m generally feeling quite negative about startups as a solution to broad challenges in American healthcare of late. An investor once told me that I’m too pessimistic to be a good venture capitalist. That may very well be true — but I’m glad I didn’t buy any of my Thirty Madison stock options.

The whole metabolic disease epidemic in the United States occurred when our food supply changed rapidly, and we became sedentary.

Nice shout-out for GLP-1 Digest! I don't know about being too "pessimistic." I think words like pessimistic/optimistic are value judgments. It's possible to be enthusiastic that a health product or service can have be valuable but the question in health is: within what system? The current structure is a kind of rock, paper, scissors, zero-sum game that forces startups to bend to status quo payment rules or suffer limited potential to grow. It's the mismatch between how the system works and the science of the problems that drive disability/cost that limits startups' potential.