Advanced manufacturing in drug supply chains

And readiness

In October 2019, Janet Woodcock, then the Director of the Center for Drug Evaluation and Research, testified before the House Committee on Energy and Commerce. “The United States, through its investment in biomedical research, has become a world leader in drug discovery and development, but is no longer in the forefront of drug manufacturing,” she wrote in her testimony. “Historically, the production of medicines for the U.S. population has been domestically based. However, in recent decades, drug manufacturing has gradually moved out of the United States.”

A little more than a year later, the onslaught of Covid revealed how prescient Woodcock’s testimony was.

The U.S. did indeed discover and develop, with stunning speed, two highly effective vaccines. But as supply chains—from furniture to car parts—staggered under manufacturing shutdowns and shipping disruptions as a result of the pandemic, the U.S. drug supply was no exception. A report published by Johns Hopkins University recorded no fewer than 33 drug shortages between late February 2020 and November 2020 (when the report was released).

Even as Covid receded, the winter of 2022-2023 brought a wave of respiratory illnesses, which many media outlets referred to as the “tripledemic,” including RSV, which disproportionately affects infants. Basic medications, including children’s Tylenol and other fever-reducing drugs, were gone from shelves.

How did this happen? And, more importantly, what now?

Fragmentation

I’ve written a lot about supply chains, mostly around the COVID vaccine rollout, and mostly focused on hospitals’ strategies for managing their own supply chains. The TL;DR is that over the last few decades, thanks to a combination of global manufacturing, environmental concerns, the advent of the intermodal shipping container, and a whole lot of geopolitics (which I’m skipping over because I don’t want to get emails about how I missed something in this purposely short summary), supply chains have become fragmented.

As Flexport’s Ryan Petersen told a16z’s Das Rush in November 2022*:

The fundamental problem in supply chain is that we’re a chain. There’s many companies. In fact, on a typical transaction where we’re moving, let’s say, a pallet of goods, a cubic meter of goods, from a factory in, pick a city—in Hangzhou, China to St. Louis, Missouri. On a transaction like that, you’ll have at least 12 companies that either touch the goods physically or are involved providing capital, like trade finance, or a letter of credit, cargo insurance, bank payments. At least 12, and as many as 20 companies, are involved in that transaction. You get information bottlenecks.

This happens with prescription and over the counter drugs too.

One positive side effect is that many drugs are actually extremely cheap. Most common generic medications, including many antibiotics, statins, and other frequently prescribed generics, are often pennies per pill.

But in gaining rock bottom prices,** we’ve lost control over some critical pieces of the supply chain.

Supply chains are distributed overseas…

Some 86% of the APIs (active pharmaceutical ingredients, the substance(s) that make the drug pharmacologically active) used in drugs intended for the U.S. market are produced abroad. However, as Woodcock testified, it’s impossible to precisely determine our reliance on other countries (and what those other countries might be) because drug manufacturers are only required to list the names and addresses of suppliers they are using—not the percentage of their business handled by that supplier, or which drugs that supplier is producing.

Of course, where the APIs are produced may become an increasingly pressing issue in an era of great power competition, particularly with regard to China. The Chinese API manufacturing base is large (per this 2019 NBER working paper, there are more than 7,000 base ingredient manufacturers), diversified, and fragmented. While the Chinese FDA (SFDA) has been devoting more resources to ensuring quality control, pressure on Chinese manufacturers to produce reliably safe drugs is a relatively recent phenomenon.

…and quite fragmented

Lengthy supply chains are also a resiliency issue. Many manufacturers use a “just-in-time” process, which means they only have as much inventory as they can immediately use. This keeps businesses from having expensive inventory on the books, but it also means that any disruptions—from a tsunami, to a plant closure, to a respiratory illness spreading in a Wuhan market—reverberate throughout the system.

It also means that if there’s suddenly a need for more medication than predicted—as with, say, an especially severe outbreak of RSV—children’s Tylenol is nowhere to be found.

Advanced manufacturing

So what now?

As with most major undertakings, the answer is probably found somewhere amid private innovation and public regulation. On the private side, the biggest unlock seems to be in advanced manufacturing, which FDA defines as a “collective term for new medical product manufacturing technologies that can improve drug quality, address shortages of medicines, and speed time-to-market.”

The most sci-fi of the advanced manufacturing techniques is 3D printing of drugs.

Most of the 3D printing applications ooze cool potential but are unlikely to be realized at scale anytime soon, especially because the use cases aren’t necessarily aimed at reducing shortages, but instead improving on the existing market for individual people. These applications include printing an antibiotic drug tailored to a child’s color and shape preferences, or printing one pill that includes all of a geriatric patient’s medications.

Adding to the sci-fi factor, Leroy Cronin of the University of Glasgow has spent some of his time (when he’s not talking about assembly theory and aliens) developing a 3D printer for universal chemical synthesis, with an obvious outgrowth of 3D printing drugs.

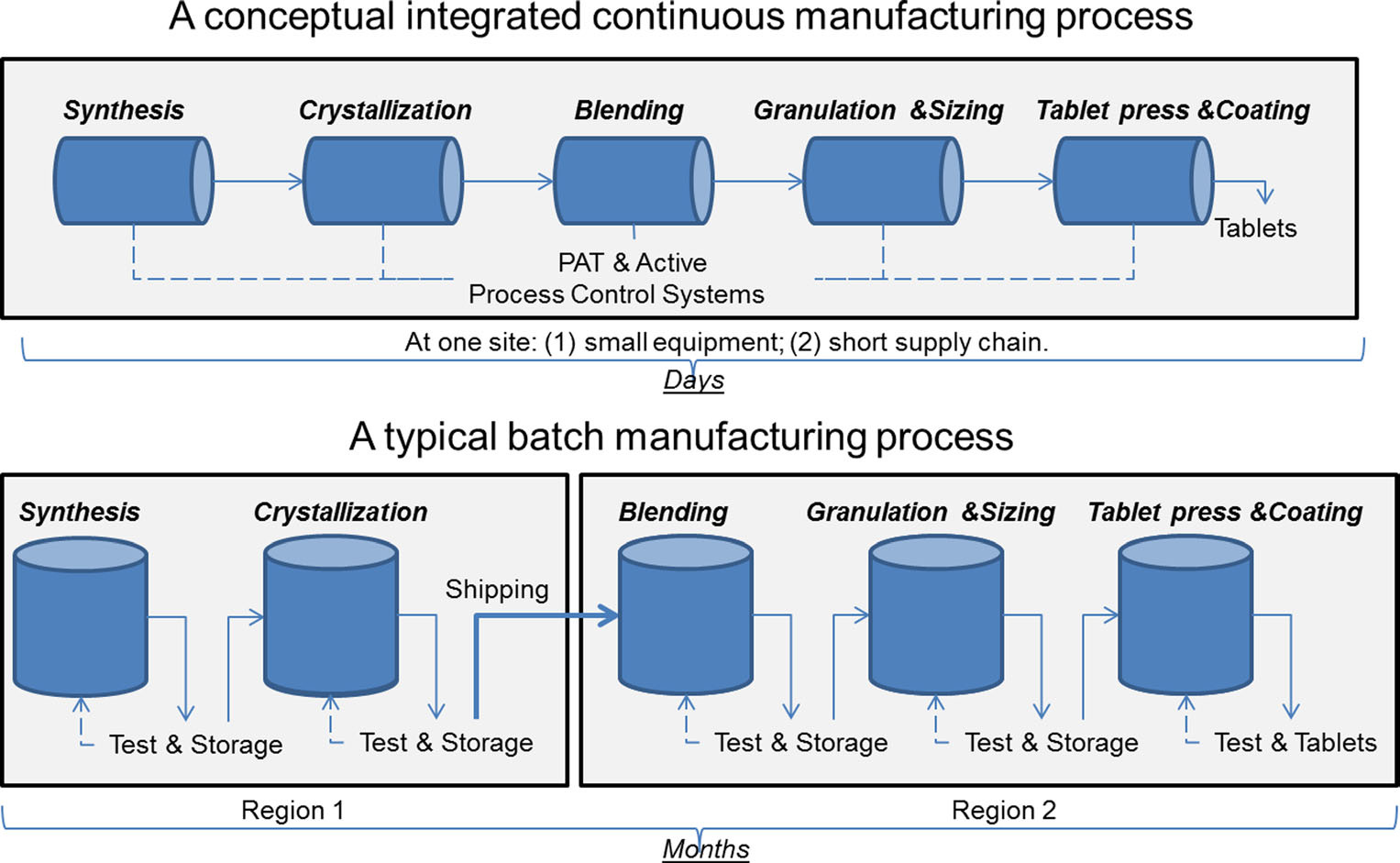

Less thrilling but more realistic in the short term is continuous manufacturing. Rather than drugs being produced in batches, as most currently are, continuous manufacturing is, as the name suggests, a continuous process. FDA has produced copious materials about how continuous manufacturing is faster, more agile, more reliable, and produces less waste—including this illustrative graphic:

Switching from batch to continuous manufacturing en masse, though, is a slow process. FDA is slowly changing its regulations, while manufacturers slowly experiment with continuous manufacturing for relevant drugs. Despite this, the field is promising. FDA approved the first application for a drug produced through continuous manufacturing in 2015, and in an FDA self-audit published in June 2022, the agency found that drugs produced with continuous manufacturing experienced a shorter time to marketing and approval. (Although it’s worth noting that the n is small, and all 5 applicants had engaged with CDER’s Emerging Technology Program, which FDA notes “may have supported first-cycle approvals.”)

Pharmacy on Demand

Also on the executive branch side, the Biden administration has taken some steps toward quantifying the problem. In February 2021, the admin signed an EO (executive order) calling for a 100 day review of critical supply chain weaknesses. The resulting report was released in June 2021, announcing, among other things, the commencement of a consortium to develop a list of 50-100 drugs to onshore. Simultaneously, HHS announced $60M to develop “novel platform technologies.”

Meanwhile, the Center for Drug Evaluation and Research (CDER) and the Biomedical Advanced Research and Development Authority (BARDA), subsets of the FDA and HHS, respectively, are collaborating on an initiative called “Pharmacy on Demand.” In her testimony, Woodcock explained this process as the “strategy and new regulatory framework to develop and implement miniature, mobile manufacturing platforms (‘Pharmacy on Demand’) for manufacture of essential drugs near or at the point of care.”

This work seems to mostly include small-scale continuous manufacturing, from API to final drug form all at once. It’s hard to find detailed information on this program, mostly because it appears to be distributed between the federal level (DARPA is involved), the university level (I found mentions of Virginia Commonwealth University and MIT, in particular), and startups. The most recent update I could find is this Pharm Tech article from April 2021.

Additional options

There are many other legislative options as well. The FDA could require more thorough API reporting (Woodcock recommended this in her testimony) from manufacturers. The Bayh-Dole Act of 1980 has a never-yet-used provision allowing federal agencies to exercise “march-in rights” and use the research it has sponsored at universities, regardless of patents. (Needless to say, this is controversial—the Congressional Research Service produced a very thorough report on the topic in 2016, which is the best down-the-line explanation I’ve found).

There could be some kind of program or assistance for individual hospitals, which often struggle with shortages and gaps in distribution even when a drug isn’t nationally in shortage. There’s the Defense Production Act, which many presidents have invoked since its passage in 1950, including Presidents Trump and Biden in response to COVID. I’m sure there’s many more options I’m neglecting, but those are the major hits.

Conclusion

Covid exposed the cracks in the U.S. healthcare system and drug procurement chain. But as we move farther out from the phase of acute illness and back to normal lives, those cracks still haven’t been filled in. The slow process of moving to advanced manufacturing is under way—but being ready for anything is going to require participation from private and public entities.

This information shouldn’t be taken as investment advice (obviously), and the opinions expressed are entirely my own, not representative of my employer or anyone else.

Please also see a16z.com/disclosures for additional relevant disclosures.

*I work at a16z. I wasn’t involved in this interview. I am a fan of our content. You should check it out.

**I know, too often the patient pays much more than those rock bottom prices—that’s Mark Cuban’s whole business model.